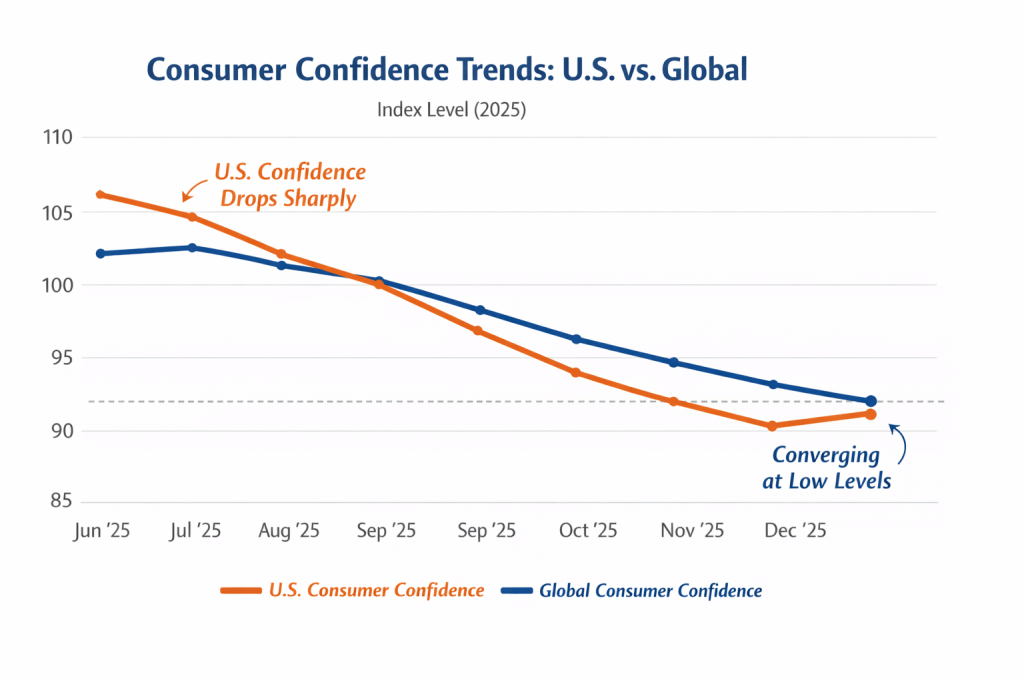

As 2025 draws to a close, one economic indicator is sending a clear signal of unease across American households: U.S. consumer confidence has fallen in December. While headline economic numbers may still suggest resilience, consumer sentiment tells a more nuanced and cautious story—one shaped by concerns over jobs, inflation, and personal financial security.

Consumer confidence is often described as a “soft” economic indicator, but its impact is anything but soft. It directly influences how people spend, save, and plan for the future. When confidence falls, it can slow economic momentum, making this decline particularly important as the country heads into 2026.

Understanding Consumer Confidence

Consumer confidence measures how optimistic or pessimistic consumers feel about the overall economy and their personal financial situation. It is commonly tracked through surveys that ask people about:

- Current business and labor market conditions

- Expectations for income, employment, and economic growth

- Willingness to make major purchases such as homes, cars, or appliances

When consumers feel secure, they tend to spend more, fueling economic growth. When they feel uncertain, they pull back—often before official data shows a slowdown.

What Happened in December?

In December 2025, consumer confidence declined for the fifth consecutive month. The drop reflects growing anxiety among households, even as the U.S. economy avoids a technical recession.

Several trends stand out:

- Fewer consumers believe jobs are plentiful

- More people say jobs are becoming harder to find

- Expectations for future income growth remain weak

- Concerns about prices and affordability persist

This combination suggests that Americans are increasingly worried not just about today, but about what the next few months may bring.

The Job Market: From Strength to Uncertainty

For much of the past two years, a strong labor market helped support consumer spending. Low unemployment and steady hiring gave workers confidence—even as inflation surged.

That confidence is now eroding.

Although unemployment remains relatively low, perceptions matter as much as reality. More Americans now feel that job opportunities are shrinking. Layoff announcements in certain industries, slower hiring, and increased automation have contributed to the belief that the labor market is losing momentum.

When people feel uncertain about job security, they delay major financial decisions. This hesitation ripples through the economy, affecting housing, retail, and service industries.

Inflation Fatigue and the Cost of Living

While inflation has cooled compared to its peak, the psychological impact of high prices lingers.

Consumers are still grappling with:

- Elevated grocery and energy costs

- High rent and housing prices

- Expensive healthcare and education

- Rising insurance and utility bills

Even when inflation slows, prices rarely return to previous levels. As a result, many households feel that their purchasing power has permanently declined. Wage growth has not fully compensated for years of higher costs, leaving consumers feeling financially squeezed.

This “inflation fatigue” plays a major role in declining confidence.

The Role of Interest Rates and Debt

High interest rates are another critical factor weighing on sentiment. Borrowing has become more expensive across the board:

- Mortgage rates remain elevated

- Auto loans cost significantly more than a few years ago

- Credit card interest rates are at historic highs

For consumers carrying debt, higher rates mean higher monthly payments. For those considering big purchases, financing costs act as a strong deterrent.

As a result, many households are prioritizing debt repayment and savings over discretionary spending—another sign of caution.

Why Confidence Is Falling Despite Economic Growth

One of the biggest puzzles of 2025 is the gap between economic data and lived experience.

| Economic Indicators | Consumer Reality |

|---|---|

| GDP growth positive | Living costs feel high |

| Inflation slowing | Prices still elevated |

| Corporate profits strong | Household finances stretched |

This gap explains why consumer confidence continues to fall even when the economy avoids worst-case scenarios. People base confidence on lived reality, not just statistics.

Why Consumer Confidence Matters So Much

Consumer spending accounts for roughly two-thirds of U.S. economic activity. When confidence weakens:

- Retail sales may slow

- Housing demand can weaken

- Business investment may decline

- Economic growth becomes more fragile

Confidence often acts as an early warning system. Prolonged declines can signal future slowdowns before they appear in employment or GDP data.

Implications for 2026

The December drop raises important questions about the year ahead.

For Policymakers

A sustained decline in confidence may increase pressure on policymakers to address affordability, job stability, and interest rates. Public sentiment often influences fiscal and monetary decisions, especially in politically sensitive periods.

For Businesses

Companies may need to prepare for more cautious consumers by:

- Offering value-focused pricing

- Avoiding aggressive expansion

- Strengthening customer loyalty

For Households

Consumers are likely to continue prioritizing:

- Savings and emergency funds

- Essential spending over discretionary purchases

- Financial stability over risk-taking

Final Thoughts

The decline in U.S. consumer confidence in December 2025 is not just a number—it’s a reflection of how Americans feel about their economic future. Concerns about jobs, inflation, debt, and affordability have combined to create a climate of caution.

While the economy has not collapsed, confidence has weakened, reminding us that economic health is as much about perception as performance. As the U.S. moves into 2026, restoring consumer confidence may prove just as important as sustaining growth itself.